Section 280E of the Internal Revenue Code functions less like a tax provision and more like a financial ceiling. By prohibiting standard business deductions for companies trafficking in Schedule I controlled substances, it forces cannabis operators to pay federal income tax on gross profit rather than net income - a structural disadvantage that no amount of operational efficiency fully offsets. Employee stock ownership plans, long a fixture of mainstream small-business succession planning, have emerged as one of the more sophisticated responses the industry has developed to work around that ceiling.

How the ESOP Structure Actually Shifts the Tax Burden

Congress created ESOPs in the 1970s as tax-deferred retirement plan trusts designed to promote employee ownership. For cannabis, their appeal is more immediate. An ESOP doesn't repeal 280E - nothing short of rescheduling or congressional action does that - but it can eliminate the entity-level tax burden for S Corporations structured the right way.

Here's the mechanism: an S Corporation's income passes through to its shareholders. If an ESOP trust owns the S Corp, and that trust is tax-exempt, the income that flows to the trust escapes federal taxation. At 100 percent ESOP ownership, the entity-level federal income tax disappears entirely. For a cannabis operator already absorbing 280E's deduction restrictions, that's not a marginal benefit - it's a structural reset of the cashflow equation.

C Corporations don't get the pass-through advantage, but they can still reduce taxable income by deducting qualifying ESOP contributions, which softens the blow somewhat. The compliance requirements attached to both structures are real. S Corp ESOPs must follow prohibited allocation rules that restrict certain highly compensated employees and family members from holding disproportionate synthetic equity interests in the plan. Participants pay ordinary income tax on distributions at retirement. The architecture isn't simple, and the transaction costs to set one up are not trivial.

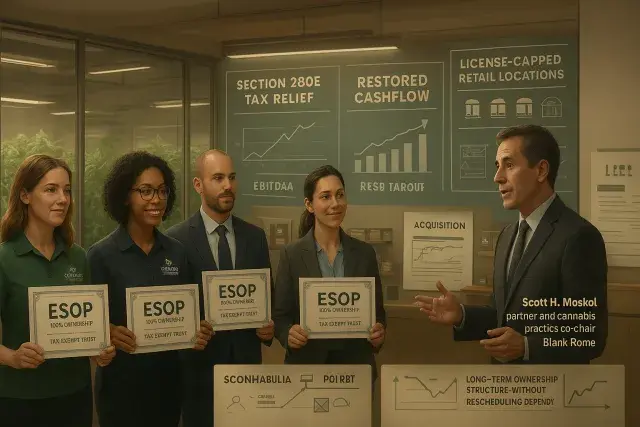

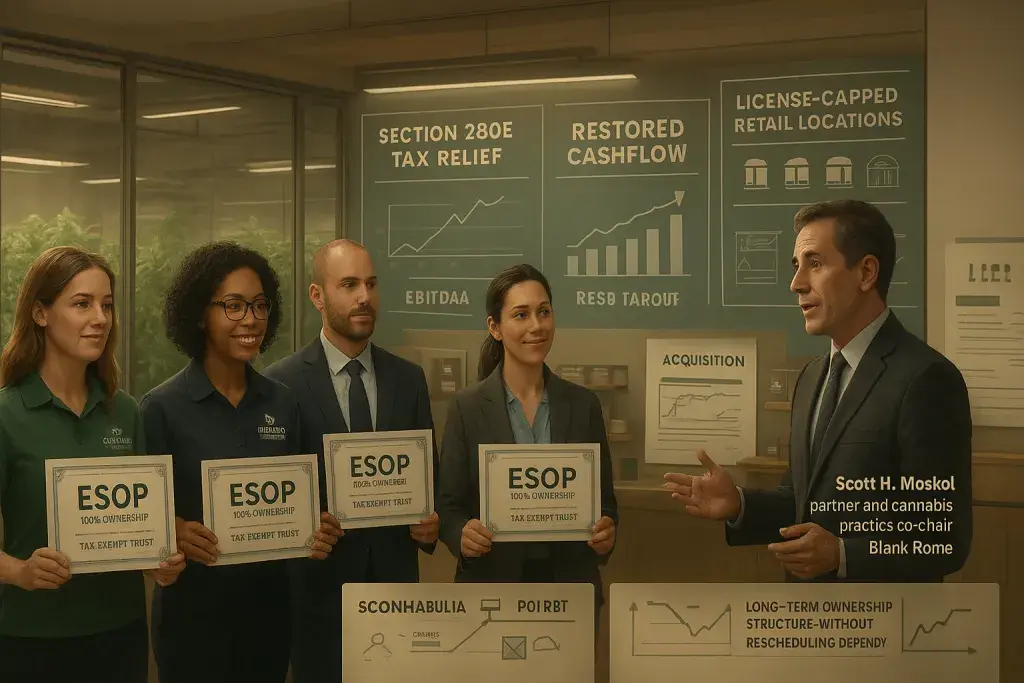

Scott H. Moskol, partner and cannabis practice co-chair at Blank Rome, described ESOPs as "especially salient for the cannabis industry" because they effectively restore cashflow that 280E would otherwise strip out. Massachusetts operators Canna Provisions and Theory Wellness have completed ESOP transactions and continue to operate. Illicit, backed in an ESOP transaction by a lender affiliated with Moskol's firm, is now using freed-up cashflow to pursue strategic acquisitions - precisely the kind of capital deployment that 280E would have made far more difficult before the structure was in place.

The freed cashflow doesn't have to go toward acquisitions. Operators can use it to pay down debt, invest in real estate currently being leased, shore up compliance infrastructure, or strengthen EBITDA heading into a future sale or institutional financing round. In an industry where traditional capital markets remain largely inaccessible, recovering cashflow from within the tax structure carries real weight.

The Non-Tax Case - Which Holds Up Even Without 280E

Here's what often gets overlooked in the 280E conversation: ESOPs solve problems that rescheduling won't fix.

In states where retail license caps constrain consolidation, the buyer pool for cannabis businesses is structurally thin. Massachusetts, for example, maintained a "three cap" on retail licenses - meaning no single operator could control more than three locations. As Moskol explained, that creates "an artificially low number of potential buyers," and an ESOP sidesteps the problem entirely by allowing a business to essentially sell to itself. No cap concerns. No concentration review. No waiting for a compliant acquirer to materialize.

The access-to-capital problem compounds this. Many operators who might otherwise pursue acquisitions lack the bank financing or balance sheet to execute traditional buyouts. Cannabis lending remains constrained relative to most industries, and equity-based deal structures often require sellers to accept illiquid cannabis stock as part of the consideration - which is a real deterrent for founders or family operators looking for a clean exit. An ESOP offers an alternative path.

Then there's the workforce dimension. Outside cannabis, decades of data from ESOP research consistently show that employee-owned companies tend to outperform on retention and engagement. In a highly regulated industry where experienced compliance staff, trained budtenders, and operations managers carry institutional knowledge that can't be quickly replaced, holding onto people isn't a soft benefit - it's a measurable competitive factor.

The Rescheduling Question and What It Actually Changes

The partial rescheduling picture currently on the table complicates the calculus. Medical marijuana moving to Schedule III provides some 280E relief for medical operators - but adult-use cannabis remains Schedule I in the federal framework, keeping the full tax burden in place for the majority of most operators' revenue. In states with both market types, medical typically represents only 20 to 25 percent of overall revenue, according to Moskol. That means roughly three-quarters of a typical multi-license operator's sales still face 280E until adult use follows suit.

Hearings are set to resume in June, but rescheduling timelines have slipped before, and "wait and see" has become the default posture for many operators still treating ESOPs primarily as a 280E workaround. That framing may be too narrow. For operators willing to think about the ESOP as a long-term ownership and exit structure - rather than a tax patch to be unwound after rescheduling - the strategic benefits don't expire when the scheduling status changes.

The transaction costs are high enough that an ESOP doesn't make sense for every operator. But for businesses with meaningful revenue, founders weighing exit options, or operators in license-capped states with thin M&A markets, the structure addresses real constraints that 280E didn't create and rescheduling won't eliminate. That's a different kind of durability.